How Can LCA Support CSRD?

The environmental ESRS standards (E1–E5) aim to describe a company’s actual environmental impact. CSRD sets new and higher requirements for how companies describe, measure, and follow up on their sustainability impact. In our article CSRD – What Is It?, we explain what the regulation means and how the reporting is structured. The next natural question is: how do you produce reliable and useful data that actually meets the requirements?

This is where life cycle assessment (LCA) plays a central role. It is not a requirement, but LCA can be used as practical support in CSRD work — from double materiality assessment to targets, actions, and follow-up.

Why LCA Is Relevant in a CSRD Context

CSRD aims to make sustainability reporting more comparable, transparent, and decision-relevant. This means, among other things, that companies must:

- report impacts across the entire value chain

- show actual environmental impact, not only activities and policies

- be able to justify why certain topics are considered material

LCA is an established and standardized tool (ISO 14040/44) for quantifying environmental impact from a life cycle perspective. This makes LCA particularly well suited as a data foundation for CSRD, where a holistic view, traceability, and transparency are specifically required.

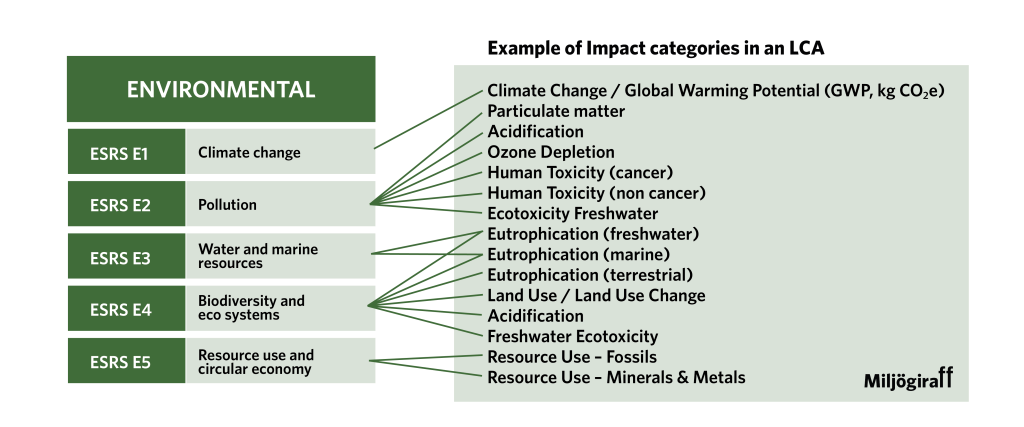

Support for Reporting According to ESRS — Especially the Environmental Standards

LCA serves as a data-based tool primarily for the ESRS E category — the environmental area. The results we obtain from a life cycle assessment through the different environmental impact categories are directly or indirectly linked to reporting points.

ESRS E1 – Climate Change

- calculate and structure climate impact in Scope 1, 2, and 3

- identify hotspots in the value chain, which is central to Scope 3 reporting

- support transition plans and climate targets with quantitative data

Through a life cycle perspective, it becomes clearer which actions actually provide the greatest climate benefit.

ESRS E2–E5 – Other Environmental Areas

Depending on the choice of method and data availability, LCA can also contribute data related to:

- waste and potential burden shifting between environmental aspects

- resource and energy use

- material flows and circularity

From Product LCA to Company Level in CSRD Reporting

LCA is often conducted at product or service level, while CSRD reporting takes place at company or group level. For LCA to be used effectively in CSRD work, these levels need to be connected in a transparent way. This is usually done by using representative product LCAs for central parts of the product range and scaling them up using volumes, purchasing data, or revenue. LCA results are often combined with other operational data to provide a more comprehensive picture of the company’s total environmental impact. Clear assumptions, system boundaries, and uncertainties are essential for the reporting to be understandable and reviewable.

LCA as Support for Targets, Actions, and Follow-Up Under CSRD

CSRD is not only about describing the current situation, but also about how companies set targets, implement actions, and follow up on their sustainability work over time. Here, LCA can serve as a central decision-support tool. By comparing different scenarios, such as material choices or energy sources, it becomes possible to quantify the effect of planned actions and prioritize the right measures. LCA also contributes to greater alignment between product development, purchasing, and sustainability reporting, making the work more strategic and less reactive.